Let’s talk about small business tax deductions. As a woman entrepreneur, this is one of those topics that can feel a bit intimidating, but mastering it is a game-changer for your financial health.

Think of it this way: a tax deduction is essentially a business-funded discount on what you owe the IRS. For every dollar you spend on a legitimate business expense, you get to subtract that dollar from your total income, which means you pay less in taxes. It’s a powerful tool for reinvesting in your vision.

Your Guide to Small Business Tax Deductions

The key to figuring out what you can and can’t deduct comes down to a simple rule from the IRS. The expense has to be both ordinary and necessary for your business.

Let’s break that down with a relatable lens.

- An ordinary expense is just what it sounds like—something common and accepted in your line of work. If you’re a graphic designer, buying design software is definitely ordinary. If you run a catering business, purchasing high-quality ingredients is an ordinary expense.

- A necessary expense is something that’s helpful and appropriate for your business. That same software is necessary for you to deliver amazing work to your clients.

It’s important to know that “necessary” doesn’t mean it has to be absolutely essential for survival. It just needs to be helpful for your operations. This simple framework is your new best friend for looking at every single business purchase with a strategic eye.

What This Means For Your Bottom Line

Getting a handle on deductions is a huge deal because it directly impacts your profitability. Every legitimate deduction you claim lowers your taxable income. That means more of your hard-earned money stays right where it belongs: in your business, funding your growth.

This isn’t about finding sneaky loopholes; it’s about being a smart, informed CEO of your own company. As your business grows, understanding your taxes becomes just as critical as your marketing plan. You can find inspiration from so many stories of women breaking barriers in small business who learned how to make their finances work for them, not against them.

The goal is to shift your mindset from simply ‘spending money’ to ‘making strategic, deductible investments’ in your business’s future. Each qualifying expense is an opportunity to strengthen your financial standing.

The government also adjusts tax rules for inflation, which affects your personal tax situation as a business owner. For the 2025 tax year, the standard deduction for single taxpayers is set to increase to $15,000, and for married couples filing jointly, it will rise to $30,000. While these are separate from your business write-offs, they are part of the overall financial picture you should be aware of. You can read more about these IRS inflation adjustments for tax year 2025 to stay on top of the changes.

To give you a clearer picture, here’s a quick look at some of the most common deduction categories you’ll encounter.

Common Small Business Deduction Categories at a Glance

| Deduction Category | What It Typically Includes | Why It Matters for Your Business |

|---|---|---|

| Home Office | A portion of your rent/mortgage, utilities, insurance, and repairs. | If you work from home, you can write off a percentage of your housing costs, turning a personal expense into a business benefit. |

| Office Supplies | Pens, paper, software, computers, printers, and postage. | These day-to-day costs add up quickly. Tracking them ensures you’re not paying taxes on money you spent just to operate. |

| Travel | Airfare, hotels, car rentals, and 50% of meal costs for business trips. | It allows you to expand your business reach without shouldering the full travel cost yourself. |

| Vehicle Use | Costs of using your car for business, based on either actual expenses or the standard mileage rate. | Whether you’re driving to meet clients or pick up supplies, these miles are deductible and can lead to significant savings. |

| Salaries & Wages | Payments to employees, including salaries, bonuses, and commissions. | This is one of the largest deductions for businesses with a team, directly reducing your taxable profit. |

| Insurance | Premiums for business liability, health insurance for employees, and other professional policies. | Protects your business from risk while also providing a valuable tax write-off. |

| Professional Fees | Money paid to lawyers, accountants, or consultants for business-related advice. | The cost of getting expert help to run your business better is itself a deductible expense. |

These categories are just the beginning, but they cover the essentials for most small businesses. The more you know, the more you can save—a key part of building a financially healthy and sustainable company.

Uncovering Deductions in Your Daily Operations

Here’s a powerful insight: many of the best tax deductions aren’t buried in some dense legal textbook. They’re hiding in plain sight, right in your daily business activities. The trick is to start thinking less about ‘spending money’ and more about making smart, deductible investments that help you grow.

Every time you make a purchase for the business, just ask yourself one simple question: “Is this ordinary and necessary for what I do?” If the answer is yes, you’ve likely found a deduction. This applies to so much more than you’d think.

For instance, your workspace is a great place to start. If you’re paying for a commercial office or a desk at a co-working space, that monthly rent is a clean, simple deduction. The same goes for your utilities—that electricity, water, and internet bill are all part of the cost of keeping your business running.

From Office Supplies to Digital Tools

Let’s break it down. The tangible and digital tools you use every day are a goldmine for deductions. These are often the easiest expenses to track because they’re frequent and clearly business-related.

- Classic Office Supplies: We’re talking about everything from the pens and planners on your desk to the printer ink and shipping boxes for your products. It all adds up.

- Software and Subscriptions: In today’s digital-first world, our tools are just as critical as a pen and paper. Your subscription to accounting software, a project management app like Asana, or even your professional email service? All deductible.

- Industry Publications: Do you subscribe to trade journals or magazines to stay on top of your game? The cost of keeping yourself informed is a valid business expense.

These are the costs directly tied to keeping your business running smoothly, making them perfect candidates for deductions that lower your taxable income.

It’s a classic mistake: entrepreneurs often brush off small, recurring expenses. But think about it—a $50 monthly software subscription is a $600 annual deduction. Tracking these consistently is one of the easiest ways to slash your tax bill.

Investing in Yourself and Your Expertise

Deductions aren’t just about the physical or digital ‘stuff’ you buy. They also cover the investments you make in your most important asset: yourself. When you grow your skills, you’re directly impacting the success and profitability of your business.

This is an area where many women entrepreneurs leave money on the table. Stop thinking of education as just personal growth—when it maintains or improves the skills your business needs, it’s a legitimate write-off.

Examples of Deductible Professional Development:

- Online Courses and Workshops: Took a digital marketing course to get more eyes on your online store? That’s deductible.

- Industry Conferences and Seminars: Attended an event to network and scope out new trends? The registration fee is deductible.

- Professional Memberships: Those annual dues for your local chamber of commerce or an industry-specific association are covered, too.

Let’s make it real. If you’re a consultant and you sign up for a certification program to boost your credibility (and your rates), that program’s cost is a deductible investment. If you run an e-commerce boutique and fly to a trade show to meet new suppliers, the costs of that trip are simply part of doing business. These expenses have a direct line to your bottom line, which is what makes them such powerful tax deductions.

Claiming Your Home Office Deduction Confidently

For so many of us, the entrepreneurial dream starts right at the kitchen table or in a spare bedroom. If your business operates out of your home, you have access to one of the most valuable small business tax deductions out there—the home office deduction. Yet, it’s also one that many business owners, especially women just starting out, feel nervous about claiming.

Let’s clear the air and get you comfortable with this powerful tool. This deduction isn’t some secret red flag for an audit; it’s a legitimate, IRS-approved way to acknowledge that your home is a real part of how you do business. By claiming it, you can turn a slice of your everyday living expenses, like rent and utilities, into major tax savings.

How to Calculate Your Home Office Deduction

When it comes to figuring out this deduction, the IRS gives you two methods. Think of it like choosing between a fixed-price menu and ordering à la carte—each has its perks, and the best one for you depends on your situation.

You can choose either the Simplified Method or the Actual Expense Method.

- Simplified Method: This is your no-fuss, straightforward option. The IRS lets you deduct a standard rate of $5 per square foot for your business space, up to a maximum of 300 square feet. That caps your total deduction at $1,500 per year. Quick and easy.

- Actual Expense Method: This one requires more attention to detail but can often lead to a much bigger deduction. You figure out the percentage of your home used for business and then apply that percentage to your actual home-related expenses.

Choosing the right method is a personal call. If you’re just getting started or prefer to keep your bookkeeping simple, the simplified method is a fantastic choice. But if you have a larger dedicated office space or live in a high-cost area, taking the time to track everything for the actual expense method will likely save you more money.

Measuring Your Space for the Deduction

Before you can calculate anything, you need to know exactly how much of your home is your office. This is step one, and it’s simpler than it sounds. The IRS requires your home office to be your principal place of business and used exclusively and regularly for your work. That “exclusive use” part is key—it means that corner of the dining room doesn’t count if it’s also where your family eats dinner.

To measure your space:

- Identify the Area: Pinpoint the exact room or defined area you use only for your business.

- Calculate the Square Footage: Grab a tape measure. A 10-foot by 12-foot room is 120 square feet.

- Find the Business-Use Percentage: Divide your office’s square footage by your home’s total square footage. So, if your home is 1,200 sq. ft. and your office is 120 sq. ft., your business-use percentage is 10%.

This percentage is the magic number you’ll use for the actual expense method. It’s what tells you what portion of your home expenses you can write off.

Tracking Actual Expenses Like a Pro

If you decide to go with the actual expense method, meticulous record-keeping is your best strategy. You’ll apply that business-use percentage (the 10% from our example) to all your qualifying home expenses.

Don’t let the fear of an audit stop you from claiming what you’re owed. The key to claiming the home office deduction with confidence is simply having great records. With clear documentation, you can easily justify your claim and maximize your savings.

Here are some of the direct and indirect expenses you can track:

- Direct Expenses: These are costs that apply only to your office space, like painting the office walls or installing custom shelving. You can deduct 100% of these.

- Indirect Expenses: These are costs for keeping your entire home running. You deduct a percentage of these based on your office’s size. Common examples include:

- Rent or mortgage interest

- Homeowners or renters insurance

- Utility bills (electricity, gas, water)

- General home repairs and maintenance

- Home security system costs

When setting up your dedicated workspace, remember that the cost of essential home office chairs and other furniture can often be included in your deductions, usually as business assets. By keeping organized records of all these costs, you can confidently claim this valuable deduction and keep more of your hard-earned money right where it belongs—in your business.

Deducting Business Equipment and Asset Purchases

Investing in the tools of your trade is one of the most exciting parts of growing a business. When you buy a new work laptop, specialized machinery for your craft, or even the perfect desk chair, these aren’t just expenses—they’re strategic investments in your company’s future. The good news? These big-ticket items come with serious tax advantages.

These larger purchases are considered business assets. You can’t just deduct them the same way you would a pack of pens. Instead of writing off the full cost in one go, you typically recover the cost over several years through a process called depreciation.

Think of it like this: if you buy a professional camera for your photography business that you expect to use for five years, the IRS lets you deduct a piece of its cost each of those five years. This approach spreads the tax benefit across the asset’s “useful life,” matching the expense to the period it helps you generate revenue.

Faster Write-Offs with Section 179 and Bonus Depreciation

Standard depreciation is a solid, reliable strategy. But what if you need a bigger tax break this year? That’s where two powerful options come into play, created specifically to encourage small business owners like you to invest in their companies right now.

- Section 179 is a game-changer for many small businesses. It lets you treat a major asset purchase as an immediate expense, meaning you can deduct the entire cost of qualifying new or used equipment in the same year you buy it and start using it. While there are annual limits, it provides a massive and immediate tax benefit for most business owners.

- Bonus depreciation is another fantastic tool for speeding up your deductions. It allows you to write off a large percentage—sometimes up to 100%—of the cost of new (and some used) assets in the very first year. The rules and percentages can change, so you’ll want to check the current year’s guidelines, but it’s another great way to get a substantial deduction right away.

Choosing between these options is a strategic move. Grabbing the full deduction now with Section 179 can dramatically lower this year’s tax bill and free up cash flow. On the flip side, spreading the deduction over several years with standard depreciation might be smarter if you expect your income to be much higher in the future and want to smooth out your tax liability.

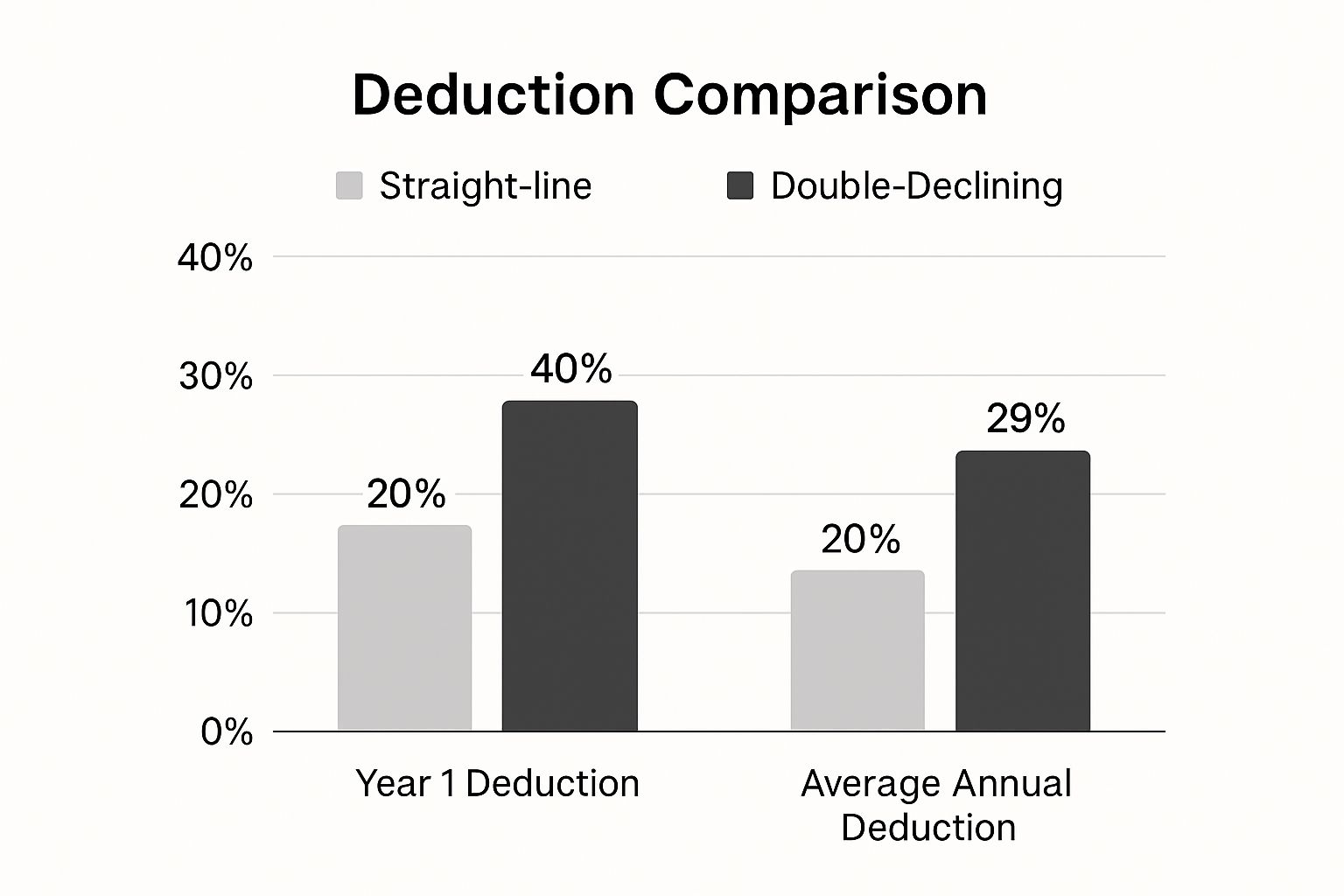

Comparing Depreciation Methods

Making sense of these different methods helps you plan big purchases with your taxes in mind. For standard depreciation, the two most common approaches are straight-line and double-declining balance. Straight-line spreads the deduction evenly over the years, while the double-declining method gives you a much bigger deduction in the early years.

This infographic breaks down how different depreciation methods affect your deductions in the first year compared to over the asset’s entire life.

As you can see, a method like double-declining gives you a much bigger tax break upfront versus the slow-and-steady pace of the straight-line method.

Deciding between front-loading your deduction with Section 179 or spreading it out is a critical choice. This table breaks down the key differences to help you decide what’s best for your business this year.

Depreciation vs. Section 179 Deduction

| Feature | Standard Depreciation | Section 179 Deduction |

|---|---|---|

| Timing of Deduction | Cost is spread out over the asset’s “useful life” (several years). | The full purchase price can be deducted in the year of purchase. |

| Deduction Limit | No annual dollar limit, but based on the asset’s cost and life. | Subject to an annual dollar limit (e.g., $1.22 million in 2024). |

| Impact on Income | Can’t be used to create a business loss. | Can be used, but only up to the amount of your business income. |

| Best For… | Businesses wanting to smooth out tax liability over time or those with low current-year income. | Profitable businesses wanting to maximize their current-year tax savings and reduce their immediate tax bill. |

Ultimately, Section 179 gives you immediate gratification by slashing your taxes now, while standard depreciation plays the long game, offering predictable deductions for years to come. Your choice depends entirely on your financial picture and strategic goals.

This idea of cost recovery is a key part of tax codes all over the world. For instance, Denmark offers a “super deduction” for R&D equipment, letting businesses write off more than 100% of the cost! These policies are designed to get businesses to invest. You can see how these kinds of global capital allowance policies work and compare them to the tools we have in the U.S.

By timing your equipment purchases and choosing the right deduction method, you can take control of your tax burden and pour those savings right back into your business.

Simplifying Travel and Meal Expense Deductions

As an entrepreneur, some of your best work happens far from your desk. Flying to a conference to sharpen your skills, driving to pitch a new client, or taking a potential partner to lunch are all part of building a business. The good news? The IRS gets it, and many of these costs are legitimate small business tax deductions.

Figuring out the rules for travel and meals can feel intimidating, but it’s crucial for claiming every penny you deserve. This isn’t just about getting a few dollars back; it’s about making smart moves to grow your business without shouldering the entire bill. Let’s break it down so you can claim these expenses with total confidence.

What Counts as Business Travel

First, for travel expenses to be deductible, the trip has to be both ordinary and necessary for your business. It also needs to take you away from your main place of business for longer than a typical workday.

This means the trip must have a clear business purpose. A weekend getaway where you happen to check a few emails isn’t going to cut it. But a trip specifically to attend an industry conference or meet with a major client? That’s exactly what the deduction is for.

When a trip qualifies, you can deduct a whole host of related costs:

- Transportation: This covers your plane or train ticket, or the cost of driving your own car to your business destination.

- Lodging: Your hotel stays or other accommodation expenses are fully deductible.

- Local Transport: Don’t forget the Ubers, taxis, or rental cars you use to get around your destination city for business meetings. They count, too.

When you’re on the road, every mile driven for business can add up to a serious deduction. Getting familiar with tax-efficient mileage tracking strategies is a fantastic way to ensure you’re capturing the full value of your business-related driving.

Navigating the Rules for Meal Deductions

Meals are a common point of confusion, but the rules are simpler than they seem. For a meal to qualify as a business expense, you (the business owner) or one of your employees has to be there. And, of course, the expense can’t be “lavish or extravagant”—so maybe skip the gold-flaked steak.

In most cases, you can deduct 50% of the cost of a qualifying business meal. This 50% limit applies to most common scenarios, whether you’re taking a client to dinner or eating alone while away on a business trip.

The most critical part of deducting any travel or meal expense is your documentation. Your mantra should be: who, what, when, where, and why. For every single meal receipt, jot down who you were with and what business you discussed. This simple habit will make your records audit-proof.

Let’s look at how this plays out in the real world:

- The Client Lunch: You take a potential client to lunch to go over a project proposal. That meal is 50% deductible because its purpose was directly tied to your business.

- The Solo Business Trip: You travel to another city for a two-day conference. The meals you eat by yourself during this trip are 50% deductible because you’re traveling for business.

- The Team Celebration: You treat your team to dinner to celebrate smashing a big sales goal. This is often 100% deductible because it falls under a different rule for employee recreation and morale-boosting events.

By understanding these key differences and keeping clean, detailed records, you can turn everyday business activities into valuable tax savings. That’s more cash freed up to pour right back into growing your company.

Creating Your System for Stress-Free Record Keeping

A tax deduction is only as powerful as the record that proves it exists. Solid record-keeping is the foundation of a stress-free tax season and the key to claiming every deduction you rightfully deserve. It’s time to build a simple, sustainable system for your business finances.

Let’s officially retire the “shoebox of receipts” method. As a busy woman entrepreneur, you need a system that works for you, not one that creates more work. The goal is to make tracking your small business tax deductions an effortless, ongoing habit rather than a frantic year-end scramble.

Ditch the Paper and Go Digital

Honestly, the easiest way to build a reliable system is by embracing digital tools. Many modern apps are designed specifically for entrepreneurs who need to manage finances on the go, and they can automate much of the work for you.

Consider using receipt-scanning apps that use your phone’s camera to capture and digitize receipts on the spot. They often pull key info like the vendor, date, and amount, and even help you categorize the expense. To make sure you don’t miss any write-offs, it’s so important to implement effective strategies to organize receipts, which will make tax time a whole lot easier.

The most impactful step you can take for your business finances is opening a dedicated business bank account. It creates a clear, undeniable line between your personal and business spending, making it incredibly simple to identify deductible expenses.

Once you have a separate account, connect it to accounting software. This lets you see all your transactions in one place and tag deductible expenses as they happen. This real-time organization is a total game-changer.

Your Essential Record-Keeping Checklist

So, what should you actually be keeping? While the specifics depend on the expense, good documentation always tells a clear story. Here’s a quick checklist of what to keep for major deduction categories.

For all expenses, you should have:

- Proof of payment (a receipt, canceled check, or bank statement will do).

- The date the expense occurred.

- The name of the vendor or person you paid.

For specific major deductions, you’ll need a bit more detail:

- Vehicle Expenses: Keep a mileage log showing the date, starting and ending odometer readings, total miles driven, and the business purpose of each trip.

- Travel Expenses: Hold onto receipts for airfare, lodging, and transportation, along with an itinerary that clearly shows the business activities planned for the trip.

- Meal Expenses: On the back of the receipt, jot down who you dined with and the specific business topic you discussed.

- Asset Purchases (Equipment, Laptops): Save the purchase receipt showing the cost and the date the asset was officially put to use in your business.

This level of detail makes your claims rock-solid. Staying on top of global tax trends is also a smart move. In 2025, many countries offer different corporate tax rates that affect how deductions are used. For example, Australia has a 25% corporate tax rate for small to medium businesses, compared to its standard 30% rate.

Building a simple but powerful system is a key step, especially if you’re transitioning from a traditional job. For more guidance on that journey, check out our guide on how to quit your job and become a full-time entrepreneur.

Frequently Asked Tax Questions

Even with the best game plan, taxes can feel like a maze. It’s completely normal to have questions pop up as you go. We get it. Here are some straightforward answers to the questions we hear most often from women entrepreneurs, designed to clear things up and give you that extra dose of confidence.

Can I Deduct the Costs of Starting My Business?

Yes, you absolutely can, but the IRS has a specific way of handling it. You can generally deduct up to $5,000 in business start-up costs and another $5,000 in organizational costs in your first year of business.

Anything over that amount gets amortized, which is just a fancy way of saying you’ll deduct it bit by bit over 15 years. Start-up costs are things you spend money on before you officially open your doors, like market research or traveling to meet potential suppliers.

How Do I Handle Expenses with Mixed Business and Personal Use?

This one comes up all the time, especially with things like your cell phone or car. The rule of thumb is simple: you can only deduct the percentage that you use for business. This is where keeping detailed records is non-negotiable.

For your car, that means a solid mileage log. For your phone, you’ll need to figure out a reasonable business-use percentage and be ready to explain how you got to that number. Your records are your proof.

It’s easy to get confused between business deductions and personal deductions. As a business owner, you will always deduct your “ordinary and necessary” business expenses on a form like a Schedule C. This is completely separate from whether you take the personal standard deduction or itemize personal expenses on your individual tax return.

Building smart financial habits is a cornerstone of success. So many self-made women have mastered these very details on their way to financial freedom, proving that knowing your numbers is power. You can learn more about the habits of self-made women millionaires to get inspired for your own journey.

At BAUCE, we’re dedicated to providing you with the actionable financial insights and community support you need to build a thriving business. Explore more expert advice and connect with fellow entrepreneurs at https://baucemag.com.