You’ve brought your dream to life. Now, let’s build the financial bedrock that will keep it thriving. Managing your business finances isn’t about intimidating spreadsheets; it's about creating a clear system to track your money, make confident decisions, and legally protect the empire you’re building. This is the foundational work that empowers you to make those big moves that lead to real growth.

Build Your Financial Foundation

Let's be real. When you're just starting out, it’s so tempting to pay for a software subscription with your personal debit card or deposit a client check into your own account. We've all been there. But mixing funds creates a messy financial picture that becomes a massive headache come tax season. More than that, it can put your personal assets at risk.

Think of this step as setting up your financial command center. Every dollar needs a job, and you need a real-time view of your company’s health. This isn't just about bookkeeping—it's about building a structure that supports your vision from day one.

Create a Legal and Financial Separation

The first, non-negotiable move is to open a dedicated business bank account. This simple action is the cornerstone of solid financial management. It guarantees that all your business income and expenses flow through one central, easy-to-track place.

Why is this so critical for you as a founder?

- Clarity and Accuracy: It makes tracking your income and expenses almost effortless. This is absolutely essential for budgeting, understanding your profit margins, and just knowing where your money is going.

- Legal Protection: If you’ve set up an LLC or corporation, keeping your finances separate protects your personal assets. We're talking about your home, your car, your personal savings—keeping them safe from business debts or lawsuits.

- Professionalism: Nothing says "I'm a serious business owner" like a dedicated business account. It signals to clients, vendors, and lenders that you’re legitimate and organized.

Open the Right Types of Accounts

Once you have that main business account, you can streamline things even more by opening a few other key accounts. This isn’t about making your life complicated; it's about creating systems that make your life easier. For a deeper look at getting your financial house in order, you can explore other expert tips to improve your finances overall.

A dedicated business credit card is another game-changer. Use it for all business-related purchases. Not only does this keep your expenses organized on one statement, but it also helps you build business credit. A strong business credit score is incredibly valuable when you need to secure a loan or get better payment terms from suppliers down the line.

As your business grows, think about opening a business savings account, too. This is the perfect spot to stash money for quarterly tax payments (so they don't sneak up on you) or to build an emergency fund. That cushion gives you peace of mind for those unexpected challenges that always seem to pop up.

To make it simple, here are the core accounts to consider setting up.

Key Financial Accounts for Your Business

| Account Type | Primary Purpose | Key Benefit |

|---|---|---|

| Business Checking | Managing daily income and expenses. | Creates clear separation and simplifies bookkeeping. |

| Business Credit Card | Paying for all business-related purchases. | Builds business credit and organizes expense tracking. |

| Business Savings | Setting aside funds for taxes or emergencies. | Provides a financial safety net and avoids tax-time panic. |

Setting up these separate accounts is more than just organizing your money. You're building a professional, legally sound operation from the ground up.

By setting up separate accounts, you're not just organizing your money—you're building a professional and legally sound operation from day one. This foundational work empowers you to make smarter, data-driven decisions as you scale.

Ultimately, putting this structure in place isn't just good business practice. It's an act of setting your business—and yourself—up for long-term, sustainable success.

Master Your Cash Flow and Budgeting

If separating your business and personal accounts is laying the foundation, then getting a handle on your cash flow is making sure your house can withstand anything life throws at it. Cash flow is simply the money moving in and out of your business. It's the lifeblood, the pulse of your company. Understanding its rhythm is what separates reactive, stressed-out business owners from proactive, strategic CEOs.

Let’s clear something up. Profit is what’s left after you pay all your bills, which is fantastic. But cash flow is what you have in the bank right now to pay your team, your suppliers, and most importantly, yourself. A business can look profitable on paper and still go under because it ran out of actual cash. This is where we get serious about managing our money.

Create a Budget That Breathes

First things first, forget those stiff, scary budgets you’re imagining. For a creative entrepreneur, a budget isn't a straitjacket; it’s a living, breathing guide that grows and changes with your business. Its job isn't to restrict you—it's to empower you to make moves with confidence.

Grab your last three to six months of business bank and credit card statements. It’s time to get intimate with your spending. You’re going to categorize every single transaction. Yes, it might feel a little tedious at first, but this is where the breakthroughs happen. You’ll uncover spending habits and patterns you never even knew existed.

- Fixed Costs: These are your non-negotiables, the expenses that show up every month like clockwork. Think rent, software subscriptions, and insurance.

- Variable Costs: This category is all about what you spend to make money. It includes things like your ad spend, raw materials for your products, or the fees you pay contractors for specific projects.

- Irregular Expenses: Think of these as the financial pop quizzes—annual insurance premiums, quarterly tax payments, or buying a new laptop when your old one finally gives out.

Once you’ve got these categories sorted, you can build a budget that looks forward. This isn’t just a wild guess; it’s an educated plan backed by your own real data.

A budget isn't a financial jail; it's your roadmap to freedom. It shows you what’s possible and gives you the green light to plan for those big goals—like hiring your first team member or launching that new service—without the anxiety of not knowing.

Track Your Cash Flow Relentlessly

Knowing your cash flow is like having a financial GPS. It tells you exactly where you are at all times so you can make smart decisions. Can I really afford this new marketing campaign? When’s the best time to invest in new equipment? Do I have enough of a cushion to get through a slow month? Tracking gives you the answers.

A simple way to get started is by creating a 12-month cash flow projection. This is basically a spreadsheet where you map out your expected income and all your anticipated expenses for the next year, month by month. This single exercise is incredibly revealing. It will immediately show you the natural seasons of your business—the ebbs and flows in your revenue.

If you run a service-based business like a consulting firm, you might notice things slow down in the summer. If you sell products, you’re probably bracing for a huge spike during the holidays. Knowing this allows you to be strategic, saving money during the boom times to comfortably coast through the slower periods. You're literally building resilience into your financial plan.

Pinpoint and Optimize Your Spending

That list of categorized expenses you made? It’s a goldmine. Now it's time to put on your detective hat and analyze it. Where is your money really going? Are there costs that have quietly crept up over the months? Any forgotten subscriptions still draining your account? We've all been there.

The goal here is to optimize, not just slash and burn. Instead of gutting your marketing budget, could you shift funds from a channel that’s not performing to one that is? Could you negotiate a better deal with a supplier you’ve worked with for years? This isn't about being cheap; it's about being strategic.

This focus on smart cost management is what helps businesses thrive long-term. Even massive corporations do this. The banking industry, for example, saw a 30% total shareholder return from mid-2023 to mid-2024, partly because they got serious about cost control and investing in the right technology. It’s a powerful lesson in how managing your finances effectively builds lasting value.

When you actively manage your budget and your cash flow, your finances stop being a source of stress and become your most powerful tool. You gain clarity, you gain control, and you gain the confidence to lead your business exactly where you want it to go.

Choose the Right Financial Tools and Technology

Let’s be real—managing your business finances doesn't mean you’re stuck with a shoebox full of receipts and a complicated spreadsheet you dread opening. Your time is far too valuable for that. The right tech isn’t just about having cool software; it’s about getting clear, real-time data so you can make smart moves for your business.

Think of your financial tech stack as your secret weapon. It’s the behind-the-scenes system that works for you, giving you back precious hours and providing the clarity you need to lead with confidence.

From Manual Mess to Automated Success

Manually tracking every single invoice, receipt, and payment is a recipe for burnout. It’s tedious, and it’s exactly where tiny errors can slip in and create massive headaches down the road. This is where financial software becomes a total game-changer, especially for us entrepreneurs where we're already wearing multiple hats.

The right tools can take over the repetitive tasks, freeing you up to focus on what you actually love—growing your business. This isn't about being lazy; it's about being strategic. Data shows that 32% of finance leaders are worried about the accuracy of their own data, because they know it’s the bedrock of good decision-making. By setting up the right systems, you solve this problem from day one.

By embracing the right technology, you’re not just saving time; you’re investing in accuracy. You're building a reliable financial nervous system for your business, one that gives you the trustworthy insights needed to scale with confidence.

Building Your Perfect Financial Tech Stack

Your "tech stack" might sound fancy, but it's really just the collection of tools you use to manage your money. The goal is to find software that actually fits your business, whether you're selling handmade goods online or offering consulting services.

Here’s what you should be looking at:

- Accounting Software: This is the heart of your financial system. Platforms like QuickBooks, Xero, or FreshBooks connect directly to your business bank account, automatically categorizing transactions and creating those all-important financial reports.

- Invoicing and Payment Processors: If you’re a service-based entrepreneur, you need a smooth way to bill clients and get paid. Tools like HoneyBook or Stripe Invoicing make it easy to send professional invoices and accept online payments without the back-and-forth.

- Expense Tracking Apps: Say goodbye to that pile of faded receipts. Apps like Expensify or Dext let you just snap a picture of a receipt with your phone, and the software pulls out all the important info for you.

To really connect all these pieces and free up your time, mastering financial workflow automation is key. It helps these different tools "talk" to each other, creating a seamless process from the moment you send an invoice to when the money hits your account.

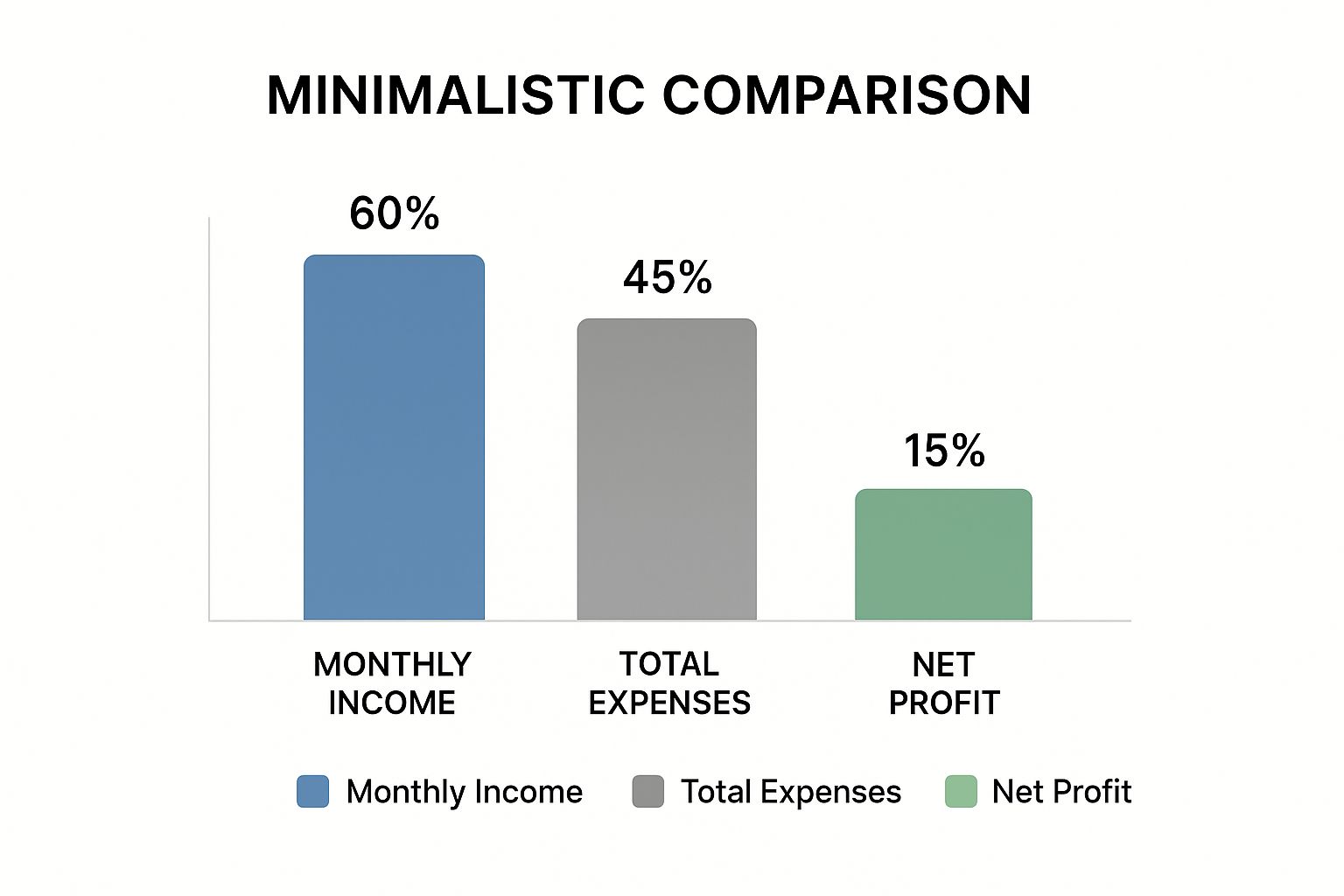

The image below shows the core metrics you'll be able to track effortlessly once you have the right software in place.

As you can see, a healthy business is one where income is consistently higher than expenses, leaving you with a strong net profit. That's the goal.

Comparing Popular Accounting Software for Small Businesses

Picking the right accounting software can feel overwhelming, but it doesn't have to be. This table breaks down some of the top options to help you see what might work best for your business needs and budget.

| Software | Best For | Key Feature | Starting Price |

|---|---|---|---|

| QuickBooks Online | Most businesses, from solo to small teams | Comprehensive features and scalability | ~$30/month |

| Xero | Service-based businesses & those with inventory | Unlimited users and project tracking | ~$15/month |

| FreshBooks | Freelancers and service providers | Excellent invoicing and time tracking | ~$19/month |

| Wave | Solopreneurs and very small businesses | Free accounting, invoicing, and banking | $0 (Free) |

Remember, the "best" software is the one that you'll actually use. Don't be afraid to test a few out before committing.

Making the Right Choice for Your Business

With so many options, how do you even choose? Don't get paralyzed by the possibilities. Start by pinpointing your single biggest financial headache. Is it keeping up with expenses? Chasing down late payments? Dreading tax season prep? Let that problem guide your first investment.

Most of these tools offer free trials, so take full advantage of them. See which one feels the most natural and intuitive to you. The best software is the one that doesn't feel like a chore to use. And remember, your tools can grow with you. You might start with a simple, free invoicing tool today and upgrade to a full accounting suite as your empire expands.

Before you spend a dime, creating a budget is the first step to understanding what you can afford and what you truly need. For a detailed walkthrough, check out our comprehensive budgeting guide. It will help you make an informed decision on which tools are a worthy investment. Choosing the right technology is a powerful act of self-investment that pays dividends in time, accuracy, and most importantly, peace of mind.

Implement Smart Tax and Profit Strategies

Let’s talk about two words that can make any business owner’s palms sweat: taxes and profit. It’s so easy to push these to the bottom of the to-do list, but getting a handle on them is absolutely essential for building a business that lasts. The great news? You don’t need a CPA license to build smart, sustainable financial habits.

This isn’t about just getting through tax season without a panic attack. It’s about creating a system that keeps your business healthy and, more importantly, makes sure it serves you. When you make tax planning a regular part of your routine and intentionally build for profit, you create a company that not only sustains itself but also fuels your own financial well-being.

Make Tax Planning a Year-Round Habit

Honestly, the best way to kill that end-of-year tax dread is to stop treating it like a once-a-year disaster. Think of it as an ongoing business activity, just like marketing or client work. This all starts with one simple but game-changing habit: setting aside money for taxes with every single payment you receive.

The easiest way to do this is to open a separate business savings account just for taxes. Seriously, do it today. Every time a client pays you or you make a sale, immediately move a percentage of that money into your tax account. A good starting point is 25% to 30% of your gross income, though this can change depending on your business structure and where you live.

This simple move accomplishes two powerful things. First, it guarantees the money is sitting there when it’s time to pay your quarterly estimated taxes, turning a stressful scramble into a simple bank transfer. Second, it gives you a much clearer, more realistic picture of the cash you actually have available to run the business.

Think of your tax savings account as a non-negotiable bill, right up there with your rent or software subscriptions. By funding it consistently, you’re paying your future self and making sure a surprise tax bill never catches you off guard.

Understand and Track Your Deductions

Let’s get into the good stuff: deductions. These are all the costs of running your business that you can subtract from your income, which lowers the amount of tax you owe. As an entrepreneur, almost everything you spend to operate and grow your business is a potential write-off.

Get in the habit of tracking these expenses like a hawk. You can use accounting software, a dedicated app, or even a detailed spreadsheet—whatever works for you.

Some of the most common business deductions include:

- Home Office Costs: If you have a dedicated space in your home that’s used only for business, you can deduct a portion of your rent or mortgage, utilities, and insurance.

- Software and Subscriptions: Your website hosting, email marketing platform, scheduling tools, accounting software—it’s all deductible.

- Professional Development: Any courses, workshops, conferences, or industry books that help you level up your skills are legitimate business expenses.

- Business Travel: This covers your flights, hotels, and 50% of your meal expenses when you’re traveling for work.

- Contractor Payments: The money you pay your virtual assistant, freelance graphic designer, or other independent contractors is 100% deductible.

Keeping squeaky-clean records of these expenses is non-negotiable. And when you’re not sure about something, always ask a tax professional. A good expert won’t just confirm what you can deduct; they’ll help you spot strategic opportunities you might be missing.

Prioritize Profit and Pay Yourself First

Okay, this is the most important mindset shift you can make. Your business must be profitable, and you, the founder, deserve to get paid for your brilliance and hard work. So many of us fall into the trap of paying every business bill under the sun and then just hoping there’s something left for ourselves. We're going to flip that script.

The Profit First method, created by Mike Michalowicz, is a fantastic framework for this. Instead of the old-school formula of Sales - Expenses = Profit, it flips it to Sales - Profit = Expenses.

Here’s how you can put it into practice:

- Allocate Your Income: As soon as money hits your account, you immediately divide it into different "buckets" (aka separate bank accounts).

- Owner’s Compensation: A percentage goes straight to your personal account. This is your salary, your reward for all the work you pour into your business.

- Profit: A small percentage—even just 1% to start—gets moved to a profit account. This is your reward for taking the risk of being an owner, and you should distribute it to yourself every quarter.

- Taxes: As we talked about, a percentage is set aside in your tax savings account.

- Operating Expenses: Whatever is left over is what you have available to run the business.

This system forces you to be more efficient and make smarter spending decisions because you’re operating on what’s truly available. It completely transforms your business from a cash-eating machine into an engine that generates wealth for its most important employee—you.

Plan for Growth and Financial Resilience

Handling your day-to-day finances is a win, for sure. But building a business with staying power? That requires looking ahead. It’s the shift from simply keeping the lights on to strategically planning for growth. This is how you build true financial resilience—the kind of strength that lets you handle whatever the market throws at you while still having the confidence to invest in your own vision.

It’s about more than just surviving a slow month. It means getting comfortable with your financial reports and using them to spot opportunities. You’re building a powerful, stable company that can weather an economic downturn and still have the cash to hire that first employee or launch a bold new service.

Reading the Story Your Numbers Tell

Let’s be real: your financial statements aren't just for your accountant. They are the story of your business, written in numbers. Learning to read them is one of the most empowering things you can do as a CEO. The best place to start is with your Profit & Loss (P&L) statement, sometimes called an income statement.

The P&L gives you a clear picture of your business's performance over a specific time—whether it’s a month, a quarter, or a whole year. It breaks down everything you need to know:

- Revenue: All the money your business brought in. Simple as that.

- Cost of Goods Sold (COGS): The direct costs of making your product or delivering your service.

- Gross Profit: What you're left with when you subtract COGS from your revenue.

- Operating Expenses: All the other costs of being in business (think rent, software, marketing).

- Net Profit: The famous "bottom line"—what’s left in your pocket after every single expense is paid.

When you start reviewing your P&L every month, you’ll begin to see the patterns. Is your revenue climbing month-over-month? Is that money you spent on marketing actually bringing in more sales? Is one of your services consistently more profitable than the others? These insights are pure gold. They tell you exactly where to double down and where you might need to pivot.

Build Your Business Emergency Fund

Life happens, and business is no different. A key client might pay late, a vital piece of equipment could break down, or a slow season might drag on longer than you planned. A business emergency fund is the financial cushion that turns these potential disasters into manageable bumps in the road. It’s your business’s peace of mind, sitting right there in a savings account.

Most experts suggest saving three to six months of essential operating expenses. To get this number, just look at your P&L. Add up your non-negotiable monthly costs—things like rent, payroll, software subscriptions, and insurance. That total is your one-month target.

Your emergency fund isn't just a safety net; it's a launchpad. Knowing you have that cushion gives you the freedom to take calculated risks, invest in new opportunities, and make decisions from a place of confidence, not fear.

If the total feels overwhelming, start small. Set up an automated weekly transfer from your business checking to a separate savings account. Even a little bit adds up and, more importantly, builds a powerful financial habit.

Preparing for a Complex Financial World

The global economy is always shifting, and that creates both new risks and new opportunities. Building a resilient business means paying attention to these bigger forces. Organizations like the International Monetary Fund often talk about the importance of being adaptable, especially with risks in market valuations and debt. In this environment, managing your finances means having a sharp focus on stability and forward-thinking strategies. You can check out more insights from the IMF on global financial stability to stay in the loop.

This really comes down to a few key things: diversifying your income streams where you can, keeping a healthy amount of cash on hand (your liquidity), and being smart about any debt you take on. The companies that build these habits are the ones best prepared to navigate tough times and jump on new opportunities when they appear.

As your business grows, so will your vision for its future—and your own. For many of us, building a successful business is the first major step toward creating a lasting legacy. That's where smart generational wealth planning comes into play. By making these forward-looking financial strategies a core part of how you operate, you’re not just managing money. You're building an empire designed to last.

Got Financial Questions? We’ve Got Answers.

Let’s be real, navigating business finances can feel like trying to learn a new language overnight. As you’re busy building your empire, it’s completely normal for questions to pop up. In fact, asking those questions is the mark of a smart, engaged CEO who’s serious about her success.

I hear a lot of the same concerns from women entrepreneurs who are right where you are. So, let’s cut through the noise and get you the clear, practical answers you need to move forward with absolute confidence.

What’s the Very First Thing I Should Do to Get My Finances in Order?

This is the question I get most often, and the answer is refreshingly simple. Before you do anything else, open a separate business bank account.

This one move is non-negotiable. It creates a clean, clear line between your personal money and your business money, which is the foundation for everything else. We're talking accurate bookkeeping, a less stressful tax season, and crucial legal protection for your personal assets. Think of it as the official starting point for mastering your business finances.

How Often Should I Actually Be Looking at My Numbers?

Finding the right rhythm for checking in on your finances is key. You don’t need to be glued to a spreadsheet 24/7, but you definitely can’t afford to just set it and forget it.

Here’s a schedule that keeps you informed without adding to your overwhelm:

- Weekly Check-in: Take just 15 minutes once a week to peek at your business bank balance. See what money came in, what bills went out, and what’s on the horizon. This quick glance keeps you grounded in your day-to-day cash flow.

- Monthly Review: Block out an hour at the end of each month for a deeper dive. This is your time to pull up your Profit & Loss (P&L) statement from your accounting software. Is revenue trending up? Are any expenses starting to creep up? This monthly ritual helps you spot trends and make smart pivots before small issues become major headaches.

A consistent financial check-in is like a regular health check-up for your business. The weekly glance keeps your finger on the pulse, while the monthly review gives you the strategic insight you need for long-term growth.

This rhythm turns your financial data from a source of anxiety into your most powerful tool for making confident, proactive decisions.

When Is It Time to Hire a Bookkeeper or an Accountant?

Knowing when to bring in a professional is a major boss move. It’s a sign that your business is growing and that you’re ready to invest in your most valuable asset: your time. Just know that a bookkeeper and an accountant play two very different, but equally important, roles.

A bookkeeper is your financial organizer. They’re in the trenches with you, handling the day-to-day tasks of recording transactions, categorizing expenses, and making sure your accounts are reconciled. They keep your financial records pristine and ready for action.

An accountant, on the other hand, is your financial strategist. They take the clean data your bookkeeper provides and help you see the big picture. They’re the ones you call for high-level advice on tax planning, business structure, and big-money decisions.

So, how do you know when to make the call? Here's a simple guide to help you decide.

| Professional | Consider Hiring When… | Key Benefit for You |

|---|---|---|

| Bookkeeper | You’re spending more than a few hours a month on financial admin or you feel constantly behind on tracking your money. | Frees up your time so you can focus on CEO activities and ensures your data is always accurate and ready for analysis. |

| Accountant (CPA) | You need strategic advice on tax savings, changing your business structure (like from a sole proprietor to an LLC), or planning for a big move like a business loan. | Provides expert guidance that can save you thousands in taxes and help you sidestep costly financial mistakes. |

Deciding to hire financial help is an investment in your business's future and your own peace of mind.

Can I Really Afford to Hire My First Employee?

Making your first hire is a monumental step! It’s exciting, but let’s be honest, it can also be a little nerve-wracking. This decision can’t be based on a gut feeling alone—it has to be backed by your numbers.

Before you even think about writing a job description, pull up your financials. A solid rule of thumb is to have at least three to four months of the employee’s total salary sitting in your bank account before you make an offer. This buffer ensures you can comfortably make payroll, even during a slow sales month.

And remember, the cost of an employee goes way beyond their salary. You need to budget for the full cost, which includes:

- Payroll Taxes: This is your share as the employer, typically around 7.65% of the employee's wages.

- Workers' Compensation Insurance: This is required in most states and protects your business if an employee is injured on the job.

- Benefits: If you plan to offer health insurance or a retirement plan, these are significant additional costs.

- Tools & Equipment: Don't forget about the cost of a new laptop, software licenses, or any other gear they'll need to do their job effectively.

Running these numbers will tell you not just if you can afford to hire someone, but if making that hire will be a profitable move for your business.